State Of Missouri Form 149

State Of Missouri Form 149 - • purchases of tangible personal property for resale: Retailers that are purchasing tangible personal property for resale purposes are exempt Missouri department of revenue, find information about motor vehicle and driver licensing services and taxation and collection services for the state of missouri. Purchasers for resale must have a missouri retail license in order to claim resale of taxable services in missouri. Signature signature (purchaser or purchaser’s agent) title date (mm/dd/yyyy) phone: Generally, missouri taxes all retail sales of tangible personal property and certain taxable services. Purchases by manufacturer or wholesaler for wholesale:

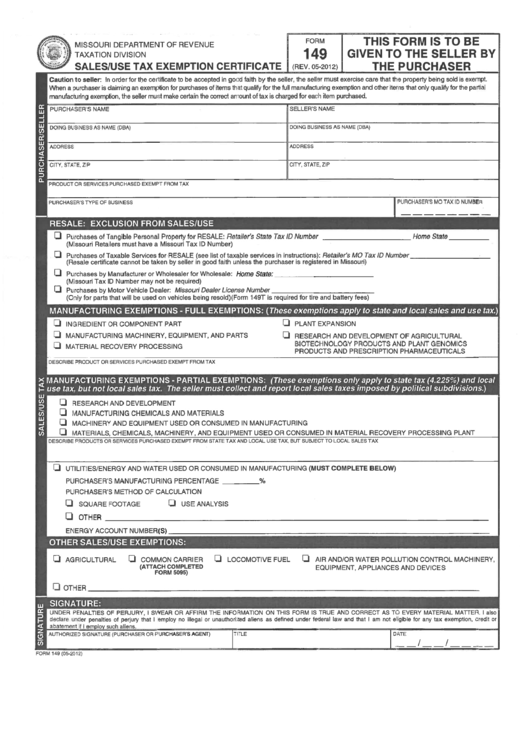

Download or print the 2023 missouri form 149 (sales and use tax exemption certificate) for free from the missouri department of revenue. Download a sales tax exemption certificate in pdf format for future use. Provide the state in which purchaser is located and registered. These only apply to state tax (4.225%) and local use tax, but not sales tax.

Retailers that are purchasing tangible personal property for resale purposes are exempt Provide the state in which purchaser is located and registered. • purchases of tangible personal property for resale: These are exempt from state and local sales and use tax. Provide the state in which purchaser is located and registered. Generally, missouri taxes all retail sales of tangible personal property and certain taxable services.

Form 149 Sales And Use Tax Exemption Certificate Edit, Fill, Sign

• purchases of tangible personal property for resale: The seller must collect and report local sales taxes imposed by political subdivisions. The seller must collect and report local sales taxes imposed by political subdivisions. Retailers.

Fillable Form 149 Sales/use Tax Tire And LeadAcid Battery Fee

Issue a missouri resale certificate to vendors for purchase of items for resale. Although exemptions and exclusions both result in an item not being taxed, they operate differently. A missouri tax id number is not.

Missouri Form 149 Fillable Form Printable Forms Free Online

Number is not required to claim this exclusion. Purchases by manufacturer or wholesaler for wholesale: Retailers that are purchasing tangible personal property for resale purposes are exempt A missouri tax id number is not required.

Missouri Form 149 Fillable Form Printable Forms Free Online

Purchases by manufacturer or wholesaler for wholesale: The seller must collect and report local sales taxes imposed by political subdivisions. Although exemptions and exclusions both result in an item not being taxed, they operate differently..

Missouri Form 149 ≡ Fill Out Printable PDF Forms Online

These only apply to state tax (4.225%) and local use tax, but not sales tax. As of today, no separate filing guidelines for the form are provided by the issuing department. • purchases of tangible.

Missouri Fillable Form 108 Application Printable Forms Free Online

All items selected in this section are exempt from state and local sales and use tax under section 144.030, rsmo. • purchases by manufacturer or wholesaler for wholesale: Provide the state in which purchaser is.

Fill Free fillable forms for the state of Missouri

All items selected in this section are exempt from state and local sales and use tax under section 144.030, rsmo. The seller must collect and report local sales taxes imposed by political subdivisions. Purchases of.

Fill Free fillable forms for the state of Missouri

All items selected in this section are exempt from state and local sales and use tax under section 144.030, rsmo. Taxable services include restaurants, hotels, motels, places of amusement, recreation, entertainment, games, athletic events, telecommunications.

Provide the state in which purchaser is located and registered. A missouri tax id number is not required to claim this exclusion. • purchases of tangible personal property for resale: Download or print the 2023 missouri form 149 (sales and use tax exemption certificate) for free from the missouri department of revenue. Generally, missouri taxes all retail sales of tangible personal property and certain taxable services.

Taxable services include restaurants, hotels, motels, places of amusement, recreation, entertainment, games, athletic events, telecommunications Missouri department of revenue, find information about motor vehicle and driver licensing services and taxation and collection services for the state of missouri. Retailers that are purchasing tangible personal property for resale purposes are exempt Purchases by manufacturer or wholesaler for wholesale:

Issue A Missouri Resale Certificate To Vendors For Purchase Of Items For Resale.

Download or print the 2023 missouri form 149 (sales and use tax exemption certificate) for free from the missouri department of revenue. Sales or use tax exemption certificate (form 149) instructions check the appropriate box for the type of exemption to be claimed according to section 144.054, rsmo These only apply to state tax (4.225%) and local use tax, but not sales tax. You can download a pdf of the missouri sales and use tax exemption certificate (form 149) on this page.

A Sales Tax Exemption Certificate Can Be Used By Businesses (Or In Some Cases, Individuals) Who Are Making Purchases That Are Exempt From The Missouri Sales Tax.

Number is not required to claim this exclusion. Missouri department of revenue, find information about motor vehicle and driver licensing services and taxation and collection services for the state of missouri. Provide the state in which purchaser is located and registered. These only apply to state tax (4.225%) and local use tax, but not sales tax.

However, There Are A Number Of Exemptions And Exclusions From Missouri's Sales And Use Tax Laws.

Download a sales tax exemption certificate in pdf format for future use. Purchasers for resale must have a missouri retail license in order to claim resale of taxable services in missouri. Signature signature (purchaser or purchaser’s agent) title date (mm/dd/yyyy) phone: Purchases by manufacturer or wholesaler for wholesale:

Although Exemptions And Exclusions Both Result In An Item Not Being Taxed, They Operate Differently.

The missouri 149 form, officially known as the sales and use tax exemption certificate, is a crucial document for businesses seeking exemptions from sales or use tax on specific items including but not limited to manufacturing equipment,. As of today, no separate filing guidelines for the form are provided by the issuing department. • purchases by manufacturer or wholesaler for wholesale: Purchases of tangible personal property for resale:

The seller must collect and report local sales taxes imposed by political subdivisions. Provide the state in which purchaser is located and registered. These only apply to state tax (4.225%) and local use tax, but not sales tax. These are exempt from state and local sales and use tax. Retailers that are purchasing tangible personal property for resale purposes are exempt